The P11D form is a critical document for UK businesses, ensuring compliance with HMRC regulations on employee benefits and expenses. Employers must submit this form to report taxable benefits provided to employees that are not processed through payroll.

For the 2024/25 tax year, the P11D deadline falls on 6th July 2025, making timely and accurate submission essential to avoid penalties. This guide covers everything businesses and employees need to know about P11D reporting, including deadlines, taxable benefits, and employer responsibilities.

What is a P11D Form Used For?

A P11D form is an essential document used by employers in the UK to report certain expenses and benefits in kind provided to employees. These benefits, which are not processed through payroll, must be declared to HM Revenue & Customs (HMRC) to ensure the correct tax is paid.

The P11D form covers a variety of taxable benefits, including but not limited to:

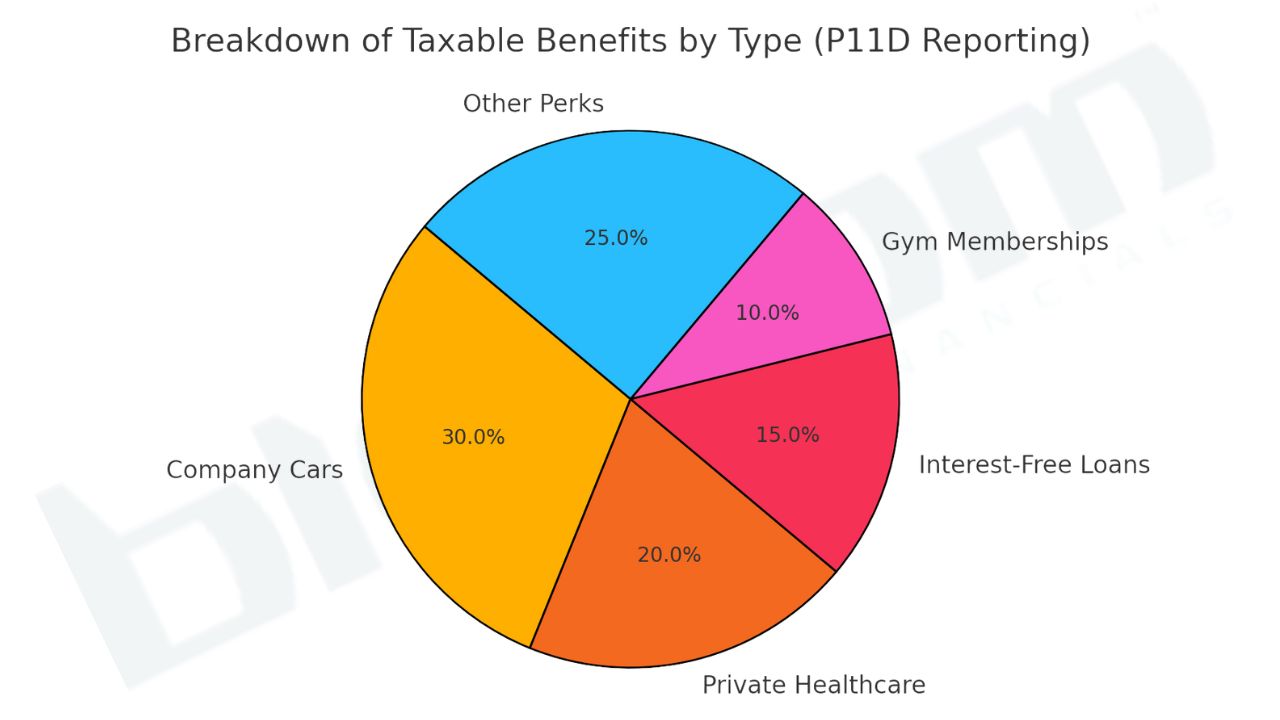

- Company cars and fuel allowances – Any vehicle provided for personal use is considered a benefit, and tax is calculated based on CO2 emissions and fuel type.

- Private medical insurance – If an employer provides health insurance, it must be reported as a taxable benefit.

- Interest-free or low-interest loans – Loans exceeding £10,000, such as those used for season tickets or personal reasons, are taxable.

- Gym memberships – If an employer pays for or subsidises a gym membership, it must be reported unless it is available to all employees.

- Relocation expenses – If an employer covers an employee’s moving costs, any amount over £8,000 is taxable.

- Employer-provided accommodation – Housing provided by an employer for employees may also be subject to taxation.

These benefits increase an employee’s overall taxable income, which may impact their Income Tax liability. It is the employer’s responsibility to ensure that all benefits in kind are accurately reported on the P11D form and submitted to HMRC before the deadline of 6th July following the end of the tax year.

P11D vs P9D and P11D vs P60 – What’s the Difference?

Many employers and employees often confuse the P11D with other tax forms, such as the P9D and P60. Below is a clear distinction:

P11D vs P9D

- The P9D form was previously used to report benefits for employees earning less than £8,500 per year.

- In 2016, the P9D was abolished, and now all benefits in kind must be reported via the P11D form, regardless of an employee’s earnings.

P11D vs P60

- A P60 is a summary of an employee’s total salary, Income Tax paid, and National Insurance contributions over the tax year.

- Unlike the P11D, a P60 does not include benefits in kind—it only reflects the total salary and deductions processed via PAYE.

Employers must ensure accurate P11D filing to avoid tax discrepancies, HMRC penalties, and compliance issues. Misreporting can result in fines and additional tax liabilities.

Understanding Taxable Benefits for Employees

Many employee benefits provided by employers are considered taxable benefits, meaning employees may need to pay tax on them. These are reported on the P11D form.

What Expenses Go on a P11D Form?

Common taxable benefits include:

- Company cars and fuel allowances

- Private medical insurance

- Interest-free or low-interest loans over £10,000

- Gym memberships provided by employers

- Relocation expenses exceeding £8,000

- Employer-provided accommodation

How is National Insurance on Benefits in Kind Calculated?

Employers must pay Class 1A National Insurance Contributions (NICs) on the taxable benefits reported in the P11D. This is charged at 13.8% of the total value of benefits provided.

P11D Working Sheets for Accurate Reporting

Employers should use P11D working sheets to ensure correct benefit calculations and avoid HMRC penalties. These working sheets help maintain clear records and streamline the submission process.

Breakdown of Taxable Benefits by Type

Here is a visual breakdown of the most commonly reported P11D benefits.

P11D Submission & Compliance

Employers must file P11D forms correctly to meet HMRC compliance requirements.

How to File a P11D with HMRC

- Prepare benefit records: Gather data on all taxable benefits provided.

- Use HMRC’s online system: Employers can file via HMRC Online Services or third-party payroll software.

- Submit before the deadline: The P11D deadline for 2025 is 6th July 2025.

When is P11D Online Submission Required?

Employers must submit P11D forms online if they employ more than 10 employees. HMRC encourages electronic submission as it speeds up processing and reduces the likelihood of errors. Online submission can be completed through HMRC’s PAYE Online Service or via approved payroll software.

For businesses with 10 or fewer employees, paper P11D forms may still be used, but online filing remains the preferred method for efficiency. Submitting forms electronically provides benefits such as:

- Instant confirmation of receipt from HMRC.

- Reduced risk of errors through built-in validation.

- Faster processing, ensuring tax records are updated promptly.

Late submission can result in penalties, so businesses should ensure timely and accurate P11D filing.

Is P11D Required for All Employees?

No, a P11D form is only required for employees who have received taxable benefits in kind. If an employee has not been provided with any reportable benefits, their employer does not need to file a P11D for them.

However, even if no P11D is required, businesses must still complete and submit a P11D(b) form to declare that either:

- No benefits were provided, or

- Class 1A National Insurance Contributions (NICs) are due on benefits provided.

Failing to submit a P11D(b) when required may result in penalties and compliance issues with HMRC. Employers should review employee benefits annually to determine whether a P11D submission is necessary.

Key Deadlines & Late Filing Consequences

Employers must comply with strict P11D deadlines to ensure tax compliance and avoid penalties from HMRC. Failure to submit on time can result in financial penalties and additional scrutiny from tax authorities.

P11D Deadline for the 2024/25 Tax Year

- 6th July 2025 – This is the final deadline for employers to submit P11D forms to HMRC, reporting any taxable benefits provided to employees.

- 22nd July 2025 – Employers must pay Class 1A National Insurance Contributions (NICs) by this date if paying electronically. If paying by cheque, the deadline is 19th July 2025.

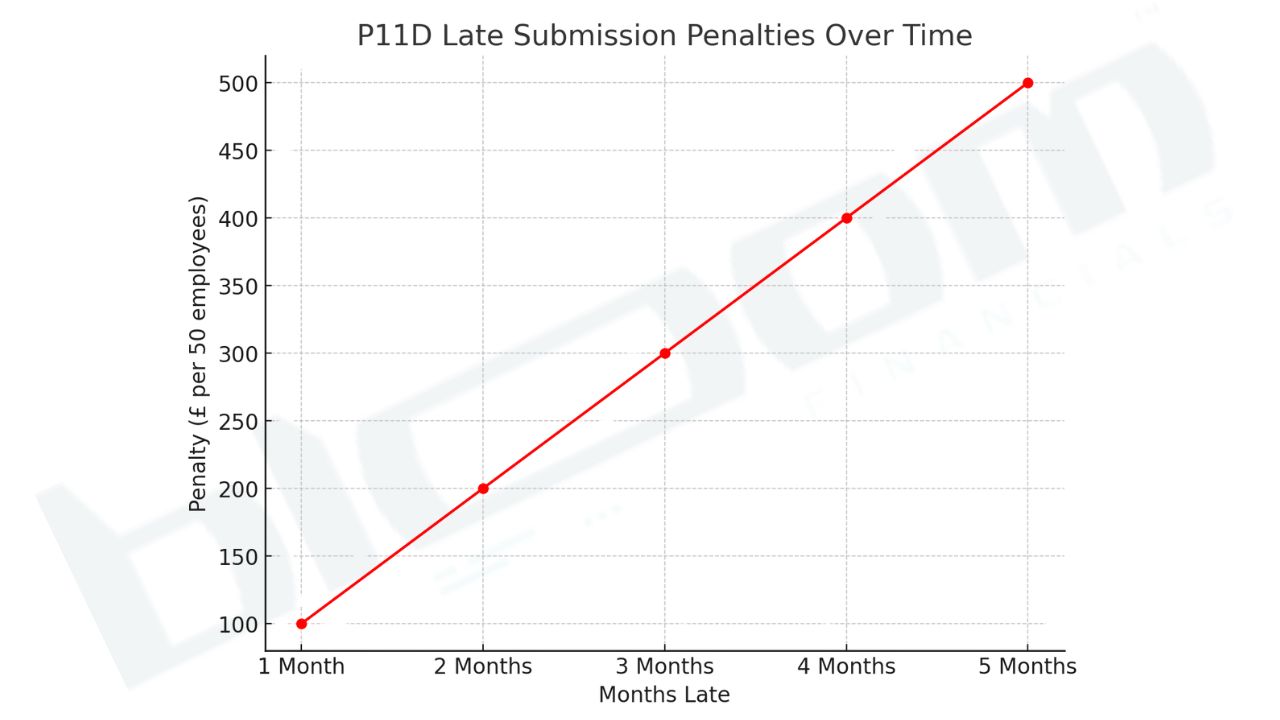

What Happens if P11D is Filed Late?

Missing the 6th July deadline can result in automatic penalties. Employers will incur a fine of £100 per 50 employees for each month the P11D is late. Additionally, if Class 1A NICs are not paid by 22nd July, HMRC may charge interest and additional fines.

P11D Penalties and Fines

- Incorrect filings: If incorrect information is submitted, HMRC can impose fines of up to 100% of the unpaid tax if they determine the error was deliberate.

- Deliberate evasion: Businesses attempting to avoid reporting taxable benefits may face severe penalties, including HMRC investigations and legal consequences.

To avoid late filing penalties, employers should prepare their P11D forms in advance and use HMRC’s online system to ensure timely submission.

Avoiding Common P11D Mistakes

Employers must be diligent when completing P11D forms to ensure compliance with HMRC regulations and avoid penalties. Even small errors can lead to fines, unnecessary tax liabilities, or HMRC investigations. Understanding common mistakes can help businesses stay compliant and reduce the risk of penalties.

How to Avoid P11D Penalties

To minimise errors and avoid HMRC fines, employers should:

- Double-check all reported benefits before submission to ensure accuracy.

- Include all taxable benefits not processed through payroll on the P11D form.

- Submit the P11D(b) form to report Class 1A NICs, even if no P11D is required for individual employees.

- Keep accurate records of all benefits in kind provided to employees throughout the tax year.

- File the P11D before the 6th July deadline to prevent automatic late filing penalties.

Common P11D Exemption Rules

Certain benefits are exempt from P11D reporting, including:

- Work-related training courses paid for by the employer.

- Employer contributions to registered pension schemes.

- Free or subsidised meals at work, provided they are available to all employees.

Do I Need to File a P11D if No Benefits Were Given?

If an employer has not provided any taxable benefits, they do not need to file a P11D. However, they must still submit a P11D(b) form to confirm to HMRC that no Class 1A NICs are due. Failing to submit a P11D(b) can result in penalties, even if no benefits were provided.

Understanding P11D vs Other Tax Forms

Employers and employees must understand the differences between P11D and other tax forms to ensure accurate tax reporting and compliance with HMRC regulations. Each form serves a distinct purpose depending on the nature of employment and tax situation.

P11D vs Self-Assessment Tax Return

- Employees receiving taxable benefits reported on a P11D form may need to include this information on their Self-Assessment tax return.

- HMRC notifies individuals if they need to complete a Self-Assessment. This is often required for high earners (above £100,000) or those with additional sources of income.

- Benefits declared on the P11D may impact an employee’s tax code, leading to tax adjustments in future years.

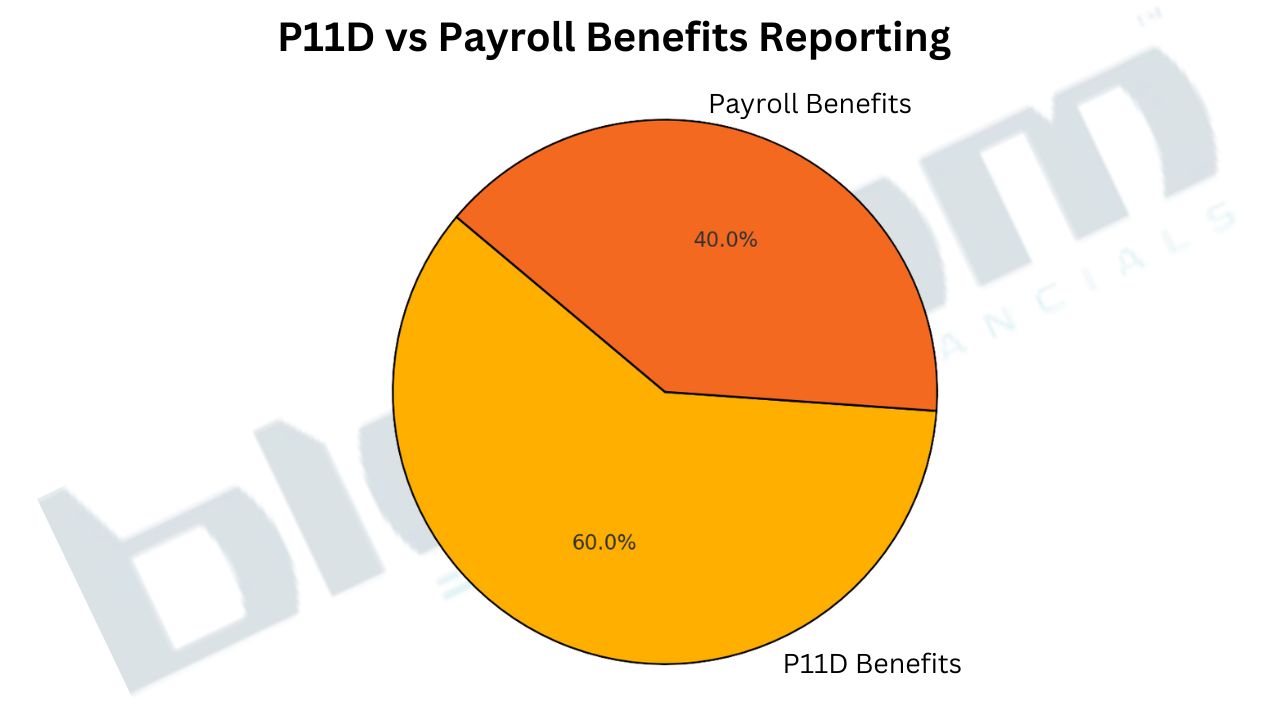

P11D vs Payroll Benefits Reporting

- Employers can process benefits through payroll, eliminating the need to submit P11D forms for those benefits.

- Payroll benefits reporting ensures tax is deducted monthly instead of being declared separately at the end of the year.

- This method simplifies tax collection for employees and reduces administrative workload for employers.

P11D vs PAYE Settlement Agreement (PSA)

- A PAYE Settlement Agreement (PSA) allows employers to pay tax on behalf of employees for certain minor, irregular, or impractical-to-calculate benefits.

- Using a PSA can help businesses avoid individual P11D reporting for specific benefits.

P11D vs P45 – When is it Required?

- A P45 is issued when an employee leaves employment, summarising total earnings and tax paid.

- Unlike the P11D, a P45 does not include benefits in kind, which must be reported separately on a P11D form if applicable.

Employer Responsibilities & National Insurance Liabilities

Employers in the UK must accurately report taxable benefits and ensure the correct National Insurance Contributions (NICs) are paid. This includes submitting P11D and P11D(b) forms and paying Class 1A NICs on taxable benefits in kind. Understanding these obligations is essential to avoid HMRC penalties and compliance risks.

What is P11D(b) Employer Liability?

A P11D(b) form is a critical document that must be submitted alongside P11D forms. While P11D forms detail taxable benefits for individual employees, the P11D(b) form is used to declare the employer’s total Class 1A NIC liability.

Key points about P11D(b) submission:

- Employers must file P11D(b) even if no P11D forms are required (e.g. if all benefits have been taxed via payroll).

- The deadline for submitting P11D(b) forms is 6th July 2025 for the 2024/25 tax year.

- Employers must pay Class 1A NICs by 22nd July 2025 if paying electronically (or 19th July 2025 if paying by cheque).

- Failure to submit P11D(b) on time can result in penalties and interest charges.

Understanding P11D Class 1A NIC

Employers must pay Class 1A NICs on certain taxable benefits provided to employees. These contributions are separate from the employee’s own NICs and are solely an employer’s responsibility.

How is Class 1A NIC Calculated?

- Class 1A NICs are charged at 13.8% of the total taxable benefit amount.

- If an employee receives a company car worth £5,000 as a taxable benefit, the employer must pay £690 (13.8% of £5,000) in Class 1A NICs.

- Employers must ensure correct calculations to avoid underpayments or overpayments.

What is Class 1A NIC on P11D?

Class 1A NIC on P11D refers to the employer’s National Insurance liability on taxable benefits. Unlike other NICs:

- Employees do not pay Class 1A NICs—only employers are responsible.

- The total amount payable is declared on the P11D(b) form.

- If Class 1A NICs are not paid by the deadline (22nd July 2025), HMRC will impose interest charges and potential penalties.

Employers must review their P11D(b) calculations and ensure timely payments to avoid financial consequences.

Special Cases & Additional Considerations

Certain P11D expenses and tax relief options require special consideration. Employers should be aware of what expenses need to be reported, how employees can reclaim tax, and how to correct errors in P11D submissions.

What are the Most Common P11D Expenses?

Many benefits in kind must be reported on a P11D form, as they impact employee tax liabilities. The most common P11D expenses include:

1. Company Cars & Fuel Benefits

- Employers must report company cars provided for personal use.

- The taxable value is based on CO2 emissions, fuel type, and list price.

- Fuel allowances (where employers cover fuel costs) must also be reported.

2. Private Healthcare Insurance

- If an employer provides private medical insurance, it is considered a taxable benefit.

- The full cost of the insurance premium must be reported on P11D.

3. Interest-Free Loans Exceeding £10,000

- Loans provided by employers with an outstanding balance over £10,000 are taxable.

- Season ticket loans, personal loans, or other advances must be reported unless already taxed through payroll.

4. Professional Subscriptions

- If an employer pays for an employee’s professional membership, it may be taxable.

- Exemption applies if the membership is required for the job (e.g., a solicitor’s Law Society membership).

Employers should keep detailed records of these benefits to ensure accurate P11D submissions.

P11D vs P87 Tax Claims – What Employees Can Reclaim

Employees who incur work-related expenses may be eligible to claim tax relief through a P87 form rather than a P11D.

What is a P87 Tax Claim?

A P87 form allows employees to reclaim tax on specific expenses that are not reimbursed by their employer.

What Expenses Can Employees Claim?

- Travel costs for business purposes (excluding commuting).

- Work-from-home expenses (e.g., energy costs, internet if required for remote work).

- Uniform or work clothing (must be a requirement for the job).

- Professional fees or subscriptions (if necessary for employment).

P11D vs P87 – Key Difference

- A P11D form reports taxable benefits that increase an employee’s tax liability.

- A P87 form is used to claim tax relief on eligible work-related expenses.

Employees must ensure they meet HMRC criteria before submitting a P87 tax claim.

Guidance on P11D Late Filing & How to Rectify Mistakes

Employers must correct P11D errors promptly to avoid fines and potential HMRC investigations.

What Happens If a P11D Is Filed Late?

- A £100 penalty per 50 employees applies for each month the P11D is late.

- Additional interest and penalties may be charged if Class 1A NICs are not paid by 22nd July.

How to Rectify P11D Mistakes

If an employer discovers an error after submission, they should:

- Resubmit the P11D with correct information using the same method as the original submission.

- Inform HMRC as soon as possible to minimise penalties.

- Adjust payroll records if necessary to correct tax deductions.

- File an amended P11D(b) form if Class 1A NICs need to be adjusted.

Key Takeaways for Employers

- Review P11D forms before submission to prevent errors.

- Use HMRC-approved payroll software for more accurate calculations.

- Keep detailed records of all taxable benefits to avoid discrepancies.

By ensuring timely and accurate P11D reporting, employers can avoid penalties, reduce compliance risks, and maintain good standing with HMRC.

Final Thoughts & Next Steps

Ensuring P11D compliance is essential for both employers and employees to avoid unnecessary fines and maintain accurate tax records. The P11D form plays a crucial role in reporting taxable benefits, and failure to submit it correctly can result in HMRC penalties.

Key Takeaways for Employers:

- Submit P11D forms by 6th July 2025 to avoid automatic late filing fines.

- Ensure accurate reporting of taxable benefits to prevent discrepancies and potential HMRC investigations.

- File the P11D(b) form and pay Class 1A NICs by 22nd July 2025 (or 19th July if paying by cheque) to avoid interest charges.

- Review payroll processes and ensure that all benefits in kind are correctly recorded throughout the year.

Next Steps to Ensure Compliance:

- Regularly review HMRC guidance to stay updated on any regulatory changes.

- Use payroll and accounting software to streamline P11D calculations and submissions.

- Conduct internal audits to check for unreported benefits and correct any errors before submission.

- Train HR and payroll teams on P11D requirements to minimise mistakes.

By preparing early and ensuring accurate reporting, businesses can avoid last-minute errors, reduce compliance risks, and stay in good standing with HMRC.